Higher Price. Thinner Floor

The market went up. The risk went with it. Here's an update on market internals.

Two weeks ago, One Accident Away laid out six reasons the market was fragile. Then it went up.

So let me start where an honest update has to start. The market has made new highs, and not one of those six pressures has structurally eased. The reactor analogy still holds. The safety systems are still degraded. The only thing that clearly changed is that the operators got more confident.

I told you it was a convergence report, not a countdown. The market climbed anyway. Higher price does not retire the risk. It raises the bill on it.

Now the part most articles like this one skip.

A bearish read of conditions is not a license to short the tape. There were no bearish trades placed through any of this. None. Price gets the final vote, and price said up. The purpose of that analysis was never to bet a macro view against the market. It was to flag when the floor underneath the price is rotting, so you are not the last one to notice when it gives way.

Conditions describe the risk. Price decides the timing. Confuse the two and the market will take your money while you are busy being right.

What changed, and what didn’t

Run the list. Two weeks of fresh data against the six frameworks.

Valuations? Worse. The Shiller CAPE and the Buffett Indicator move in one direction when price rises against the same earnings base, and that direction is up. A market priced for perfection got priced for more of it.

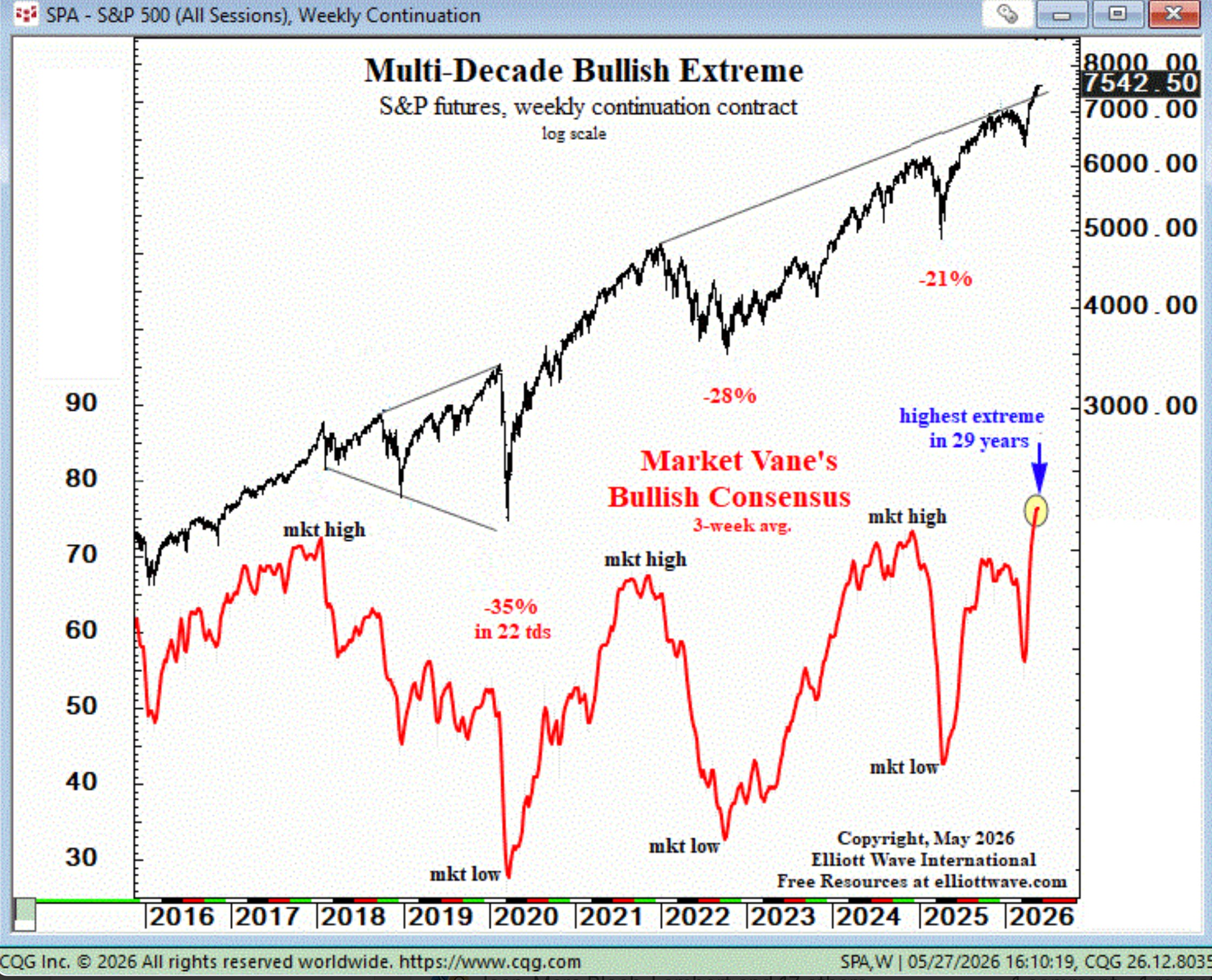

Sentiment? More extreme. The wall of worry that existed in March is now a row of confident, internally consistent theories about why the AI build-out justifies any multiple. The conversion from fear to conviction has only deepened.

Energy? The fault line printed, then partially reversed in a single week. In the original piece, the Strait of Hormuz was framework number three, a theoretical channel from a maritime chokepoint into your grocery bill. It stopped being theoretical. This week’s inflation report carries the energy shock inside it.

Yes, there is “reprtedly” news of US and Iran reportedly reaching a 60-day memorandum to extend the ceasefire and gradually restore traffic through the Strait. More on what that does and does not change below.

Inflation? Higher, but not as hot as feared. PCE rose to 3.8% year over year in April, the highest reading since May 2023, with core PCE at 3.3%. Note the market’s reaction, because it matters more than the number. The print landed roughly in line rather than above fears, and combined with the Iran news, bond yields fell rather than spiked. The Fed is now expected to hold well into next year and to raise only if inflation stays elevated. Cuts are not coming to rescue this tape. The “Fed cannot save you” framework is intact. The “inflation is about to break everything this week” framing is not.

The consumer? Running thinner. The personal saving rate fell to 2.6% in April, the lowest since June 2022, down from 4.3% at the start of the year. Americans are funding consumption out of savings they are draining.

What moved in the bulls’ favor is two things. Price structure, and a genuine de-escalation in the Gulf. Both are real. Neither repairs the six frameworks. They reset the timer.

And it’s not hard to see the bull’s point

Here is the rebuttal the original piece set up, and an honest update has to meet it head-on, because it is the bull’s best card.

The original argued that full-year earnings estimates had not been revised to reflect the world we are actually living in, with the clear implication they would be cut. They were not. The opposite happened. Forward earnings estimates have climbed roughly 14.4% year to date against a price gain of about 9.2%, which means the forward multiple compressed rather than expanded. On that one measure, the market got marginally cheaper, not more expensive.

That is the bull case in a sentence. Earnings are leading, not following.

That deserves a straight answer, not a wave of the hand, because the data is the data. Two things matter here, and they are why the verdict is not in.

First, the cost shock only reached the hard numbers this month. Margin compression shows up in earnings after it shows up in prices, and prices moved before estimates could catch it. Estimates rising ahead of input costs hitting the income statement is the sequence you would expect, not a refutation of it.

Second, the original named the test, and the test has not happened yet. The real read is forward guidance at Q2 reporting in July, against a quarter that actually contained the disruption. Q1 did not. The estimates that rose were built largely on pre-shock business activity. The number to watch is whether full-year consensus survives July, not whether it held in May.

And note what the rising estimates did not do. The forward P/E compressed from roughly 21 to roughly 20. Both readings sit above the five-year average of 19.9 and the ten-year average of 18.9. The market got slightly less expensive while remaining expensive. That is not a margin of safety. It is a smaller margin of error.

Everything to this point has been the macro update. What follows is the part that matters for a portfolio: what the internals are doing right now, what the global bond market spent May saying, and what a rules-based model did about all of it without making a single forecast.